CECL IMPLEMENTATION AND EARLY ADOPTERS

The Financial Accounting Standards Board (FASB), in June 2016, issued the Accounting Standards Update (ASU) No. 2016-13, which introduced the Current Expected Credit Loss (CECL) model. The update moves the accounting for credit losses on various financial instruments to the Expected Credit Loss (ECL) model from the existing incurred loss model. This move has impacted financial institutions such as insurance companies, banks, credit unions, and finance companies. Following the 2008 global financial crisis, the Financial Crisis Advisory Group (FCAG) suggested several improvements in financial reporting. It identified the flaws of the historical incurred loss model, which included delayed recognition of losses by financial institutions. This led to the development of CECL, the effective date for which has now been pushed back by the FASB to January 2023.

Institutions that have not been classified as smaller reporting companies have already begun implementing CECL with varying degrees of success. The volatile economic environment and limited data have made forecasting losses a challenging task, especially for smaller institutions. For companies who still have not adopted CECL, there are considerable insights to be gained from these early adopters. Most large institutions have been using complex modeling techniques and relying on multiple models, depending on the pools or portfolios. Small financial institutions can use a single model that is less complex for calculating their ECL. Many early adopters compared their existing credit loss forecasting models with the new guidance and have put into place modifications required to start implementing CECL. One such model is the vintage loss rate methodology, which uses past pools to estimate future losses.

The vintage loss rate methodology

The data required to implement the vintage loss rate methodology is collected by most financial institutions in some form. Collecting data is just one aspect of it. The real challenge lies in utilizing this historical data in the right manner to accurately predict future losses. The vintage method is especially efficient when it comes to this aspect of data utilization and analysis and comes up with allowance figures for financial institutions under CECL. Many institutions looking for the best method to use to be CECL compliant are turning towards this vintage method. There are several features, advantages, and disadvantages of this method that institutions need to be aware of before they formalize the vintage loss rate methodology to estimate their Allowance for Loan and Lease Losses (ALLL). We will subsequently discuss where this methodology fits into CECL’s overall scheme of things.

The vintage method seeks to address the FASB’s concern regarding institutions maintaining inadequate reserves due to a delay in recognition of credit losses. It seeks to factor in the below-listed information in its calculations:

- Current conditions

- Past events

- Reasonable forecasts

- Economic environment

- Quantitative and qualitative factors

Under CECL, the impetus is not so much on capturing remote and unexpected events as it is on capturing expected losses. For a given loan pool, vintage analysis calculates the cumulative loss rates to find out the pool’s lifetime expected loss. This method merges historical gross charge-off information with qualitative and environmental factors to approximate an institution’s probable and estimable future losses.

Vintage analysis in detail

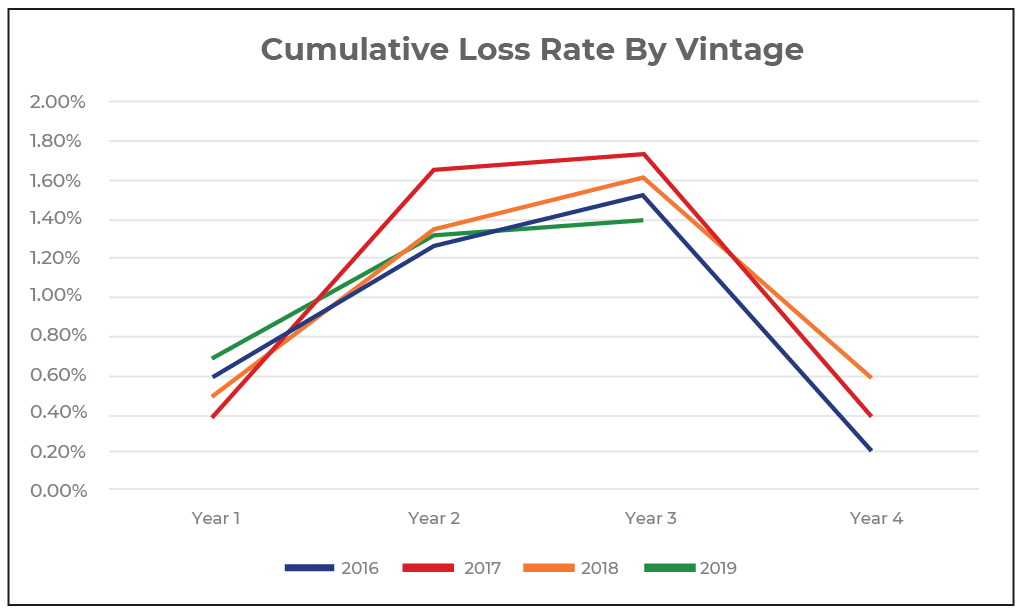

The concept of a “vintage” is central to how this method works. In vintage analysis, “vintage” is a pool of loans with the same origination period. Stratification of a given loan pool using origination periods gives a more realistic estimate of the historical lifetime loss experience. This method scores over some other CECL methods as it considers the entire life of the loan pool for its analysis and not just limited periods of time.

Let us consider the example given in the table below. It consists of four-year loan pools segmented into vintages. It calculates the life of loan loss experience and, thereby, the cumulative loss rate for each vintage. This is achieved by dividing each year’s net charge-offs by the principal balance at the time of origination. Post its origination year, the loss experience is tracked annually for the original balance for each subsequent year. This gives us the cumulative loan loss over the life of the loan. And, it is based on historical averages. The objective of vintage analysis is to forecast future loss rates by using existing data. This methodology is illustrated in the table below, where the 4th year loss rates for the 2019 vintage will be predicted based on historical loss rate trends of previous vintages with similar profiles and duration.

Qualitative factors (Q-factors) and vintage analysis

Expected loss calculations using vintage analysis also factors in macroeconomic indicators of qualitative factors. This ensures that both quantitative and qualitative data factors have been accounted for during calculations.

For example, unemployment rates frequently affect the Q-factors nationally, internationally, and at the local level. If a trend is observed wherein a shift in unemployment rates leads to an increase in charge-offs four months later, then the forward-looking loss projections are adjusted proportionately. Observing such trends in the loss history of loan pools is the basis of vintage loss rate methodology. These trends are then applied to active loan pools to predict the direction the loss rate curve may take and then set up reserves accordingly. In the example given above, it is clear that external and internal factors play a crucial role in affecting the life of loan loss experience towards the middle part (second and third year), and not so much towards the maturity period, which is the fourth year. Gathering historical data and trends is the key to expected loss rate calculations using the vintage method.

Limitations of the vintage loss rate methodology

When we set up a vintage pool, there are a few elements to consider that need to be taken care of. The setting up of this vintage pool has to properly reflect the risk profile of the loans in that pool, which we are using to do the risk assessment. Also, both pools need to have loans that go on for the same duration. Hereon, every time we report, we have to check if all factors in the pool that is being assessed are correct as this process is not automated. For example, if 1/3rd of the loans go from 0 to 30 and 30 to 60 days delinquency, all of a sudden, we have a vintage that is no longer reflective of the pool being assessed. Therefore, we have to check these pools and compare them every single time to make sure that we have got loans in both pools whose risk profiles are still the same for each reporting period. If the risk profile changes, then the bank has to go and check if there is another vintage pool available in its historical data with loans having the same life cycle and risk profile. It is clear from the example that vintage cannot be automated, and maintenance from report period to report period can be onerous. It is not always possible to create vintage pools for the purpose, as historical data or experience may not be available.

If we do not have a vintage pool to use anymore, it means that in the middle of a CECL reporting, we have to add in another methodology. A fallback method needs to be on standby, realistically, when a vintage analysis is being used. The dynamic nature of the vintage analysis needs to be kept in mind while adopting this method for CECL calculations.

CECL Express can help…

CECL Express is a turnkey solution that fully satisfies all elements of the new CECL accounting standard. The system provides all non-loan data, including:

- Yield curves and Fed data

- Linked reports on losses from the FFIEC and NCUA

- PD and LGD curves

- Macroeconomic data

Banks and credit unions need to only provide the underlying loan details for the system to provide fully auditable ECL results for multiple calculation methods, including:

- Vintage

- Roll Rate

- Discounted Cashflow

- WARM

- PD/LGD

CECL Express provides more than valid ECL results. The system computes results for all methods and all loan pools, allowing the bank to optimize its CECL configuration and avoid the worst impacts of the new standard.