CECL AND AUDIT READINESS

The Financial Accounting Standards Board (FASB) issued the credit loss accounting standard, the Current Expected Credit Losses (CECL), in June 2016. CECL focuses on expected credit losses over the life cycle of a loan and also on the reserves an institution is supposed to maintain to cover those losses. This is in contrast to the previous standard that relied on incurred losses. When implementing CECL, management will have to judge and estimate future losses. Institutions will have flexibility in developing techniques for estimating and measuring expected credit losses as long as they are consistent with the principles of the standard. Different estimation methodologies may be used by banks for different types of financial assets.

The credit loss allowance is a bank’s most important estimate and is scrutinized by auditors and regulators. For audits of financial institutions that have implemented the CECL standard, the allowance for loan losses will be considered a significant risk due to its complexity, estimation uncertainty, materiality, and sensitivity, from a user’s perspective. Auditors who audit accounting estimates need to do a high-level lookback analysis to understand the difference between actual results and previous estimates. This will help to assess the management’s process reliability.

Auditing estimates and related procedures

Procedures involved in auditing estimates include tests of the management’s methodology, evaluation of subsequent events, and tests of controls. In some instances, these procedures would also include the auditor’s independent estimate. Since the FASB has not established a standard model, auditors must be prepared to adapt their methods to the facts and conditions present at each financial institution. Auditors are also responsible for auditing-related disclosures, information about the management’s methods, and models and assumptions used in calculating the estimate.

The auditors will also look out for any management bias or irregularities in the management’s process. Under CECL, the auditor will be required to examine how much evidence is required to substantiate the allowance for loan losses. Institution-specific data would be needed to support all components of the management’s allowance for loan loss estimate, including qualitative factors. The FASB standard allows corresponding peer data to be used in certain cases where data is unavailable. The American Institute of Certified Public Accountants’ Auditing Standards Board (ASB) seeks convergence of both domestic and international rules. It has therefore proposed certain changes to its procedures for auditing estimates to align with the International Auditing and Assurance Standards Board (IAASB) revised rules.

Management can discuss their loss estimation procedures with their auditors to set up best practices under CECL. Key discussion areas to review would include the best ways to document the decision-making process and the resulting review and approval procedures. It would be prudent to always maintain records and copies of the final documentation for auditor review.

Challenges faced when providing data to auditors

Auditing an estimate has always been a challenging task, especially when it comes to bad debts. The auditor needs to consider the assumptions and methods used to calculate a CECL estimate and also, how the management’s bias can be a factor as far as estimates are concerned. The CECL standard needs more data while auditing the reserve calculations for future losses. From a preparer’s point of view, the CECL estimate is more difficult to support and govern. To meet the expectations of auditors and regulatory bodies, preparers have to increase their documentation and implement incremental controls. The five areas where auditors are expected to focus are:

- Models and methods used

- Data

- Qualitative

- adjustments Assumptions

- Controls/Governance

Data and CECL audits

Of the above factors, data is going to be the key factor that preparers can use to align their CECL estimates with those of the auditors. Most preparers initially believed that they lacked sufficient data for loss observations to prepare a relevant CECL estimate. What needs to be understood is that, besides loss history, a CECL estimate will incorporate the following data:

- Production loan data

- Historical loss conditions data

- A reasonable forecast of loss conditions

- Historical and current underwriting behaviors

- Historical and current collateral details

- Prepayment data

Preparers focus on data during implementation and while preparing an estimate. Auditors, meanwhile, focus on this data while reviewing the estimate. The aim for most preparers will be to prove the completeness and accuracy of their data during audits. They should be ready to explain any adjustments and transformations of their data. Erroneous data will also need to be cleansed from the system and missing pieces will also need to be factored in and replaced with valid assumptions. For any manipulations in data, an effective system of internal control needs to be put in place by preparers.

Certain data can be verified against a public source such as the Securities and Exchange Commission (SEC) and can therefore be deemed as transparent data. There will also be times when the data has been sourced by a vendor whose data points can be questioned for validity. In such cases, preparers will have to conduct further tests to attest to the reliability of the data.

Economic data has become an integral part of the CECL estimate, and this includes economic forecasts and historical economic data. A considerable amount of external data will be utilized for economic forecasts that are prepared internally. This data will need to be subjected to a system of internal control for its accuracy and completeness. This will ensure that preparers are more responsible for their CECL forecasts during audits.

CECL Express can help…

CECL Express is a turnkey solution that fully satisfies all elements of the new CECL accounting standard. The system provides all non-loan data, including:

- Yield curves and Fed data

- Linked reports on losses from the FFIEC and NCUA

- PD and LGD curves

- Macroeconomic data

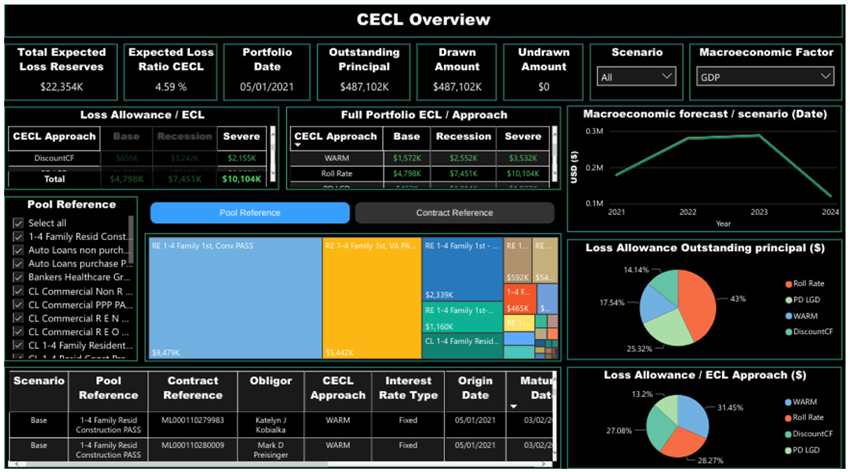

Banks and credit unions need to only provide the underlying loan details for the system to provide fully auditable ECL results for multiple calculation methods, including:

- Vintage

- Roll Rate

- Discounted Cashflow

- WARM

- PD/LGD

CECL Express provides more than valid ECL results. The system computes results for all methods and all loan pools, allowing the bank to optimize its CECL configuration and avoid the worst impacts of the new standard.