CECL AND CALL REPORTS

The Financial Accounting Standards Board (FASB) issued the Current Expected Credit Losses methodology (CECL), a new accounting standard for estimating allowances for credit losses. This new accounting standard applies to all banks, credit unions, and savings associations that file regulatory reports, which conform to the Generally Accepted Accounting Principles (GAAP) of the US. The FASB introduced CECL so that financial institutions are better equipped to tackle any situation similar to the global financial crisis. CECL replaces the incurred loss methodology and instead relies on estimating expected credit losses using various methods. These methods need historical and other data to process CECL estimates so that banks can maintain enough allowance to account for any expected credit losses. The data that is required for CECL can come from the one maintained by banks internally and also through call reports.

What are call reports?

A call report is a regulatory document that American banks are required to submit to the Federal Deposit Insurance Corporation (FDIC) on a quarterly basis. By comparing several call reports, it is possible to gather information about the health of the US banking system. A call report comprises information about the bank’s financial health.

- Call reports are quarterly financial condition reports sent to the FDIC by the US banks.

- The bank’s management must approve and verify the report’s contents.

- The size of the bank, and the capital standards applicable to it, decide its specific reporting requirements.

The call report contains several data, which are an indicator of the reporting bank’s viability. Items within the call report include:

- Bank’s income statement

- Loan information

- Deposit information

- Balance sheet investment information

- Asset sale information

- Changes in the bank’s capital

Call report submission

Financial institutions file their call reports with the Federal Financial Institutions Examination Council (FFIEC). The public can access these reports on the Federal Insurance Deposit Commission website. Call reports are used by the banking industry to find out loss information for historical periods. Future expected credit losses are then predicted using this information.

Call report limitations

But is the data contained in the call report sufficient to arrive at accurate CECL results? Several other factors influence CECL calculations that institutions need to consider to arrive at precise CECL results. These aspects are as under:

- Historical pattern in lifetime losses derived from call reports is not sufficient to arrive at accurate CECL results. We need the right economic indicator data to predict CECL allowances.

- As compared to public data sources such as call reports, the vintage or year of origination is an important data source for calculating credit losses. This vintage information, which is part of a bank’s internal data, is used as part of the Vintage Analysis Methodology to estimate losses.

- The Weighted-Average Remaining Maturity Method (WARM) calculates an average quarterly loss rate while estimating reserves under CECL. The WARM method uses the average quarterly loss rate to calculate the lifetime loss rate. Institutions that choose the WARM method should also use their internal data to subdivide portfolios by riskiness. This will help them come up with more accurate CECL results.

- While call report data may be an important source for benchmark information, the calculation of historical loss rates should involve systematic analytical capabilities that compare various approaches. This result is then considered against qualitative adjustments and economic factors to estimate future reserve levels.

- Besides historical information, CECL should consider reasonable forecasts of future events and current information along with prepayment estimates. Institutions can use various methods for estimating CECL, including probability of default/loss given default, historical loss rates, discounted cash flows, and roll-rates.

- The analysis of how historical data measures against peer experiences and industry benchmarks is important and should be given due diligence in CECL.

- Banks and other financial institutions should know the duration of their loans. They should factor in the categorization of these loans to estimate CECL and try not to be too dependent on call report data alone.

- The vintage loss rate methodology for calculating CECL allowance has to ensure that the vintage pool must reflect the risk profile of loans in the pool. This is something that call reports do not address. We will have to resort to another methodology in the middle of a CECL reporting if we do not have a vintage pool to use anymore.

- While using the WARM method, the portfolio has to be split based on riskiness. This is done so that we do not average away the risk and granularity that is supposed to be captured. Institutions, in their haste to arrive at quick and affordable CECL results, will end up using call report data, which fails to acknowledge portfolio-related factors such as granularity and riskiness. The inaccuracy of such CECL results will have severe and far-reaching consequences on institutional health.

Measuring CECL allowance accurately is a challenge for most financial institutions, and this is especially true for smaller establishments. To estimate lifetime losses, a number of different factors need to be considered. Qualitative adjustments can be made by comparing related economic indicators with historical periods of loss data. Banks must use both external and internal data for their model-based approaches while calculating CECL.

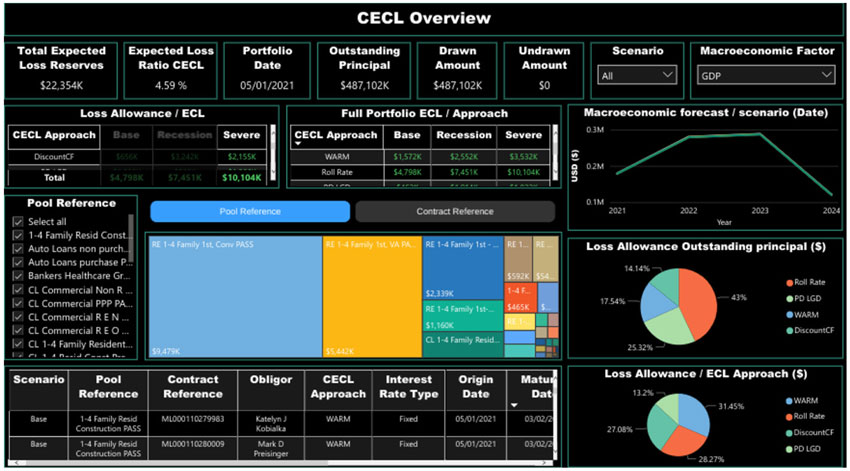

CECL Express can help…

CECL Express is a turnkey solution that fully satisfies all elements of the new CECL accounting standard. The system provides all non-loan data, including:

- Yield curves and Fed data

- Linked reports on losses from the FFIEC and NCUA

- PD and LGD curves

- Macroeconomic data

Banks and credit unions need to only provide the underlying loan details for the system to provide fully auditable ECL results for multiple calculation methods, including:

- Vintage

- Roll Rate

- Discounted Cashflow

- WARM

- PD/LGD

CECL Express provides more than valid ECL results. The system computes results for all methods and all loan pools, allowing the bank to optimize its CECL configuration and avoid the worst impacts of the new standard.