LOAN LEVEL ANALYSIS AND CECL AUDITING

Following the global financial crisis of 2007–09, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update 2016–13, also known as Current Expected Credit Loss (CECL). Using CECL, banks can proactively react to actual and anticipated changes in the credit environment by detecting expected credit losses early. The social and economic impacts of the 2020 recession were felt throughout markets, resulting in higher credit losses and a reduction in earnings and capital for financial institutions. Such turbulent times call for increased loan-level analysis of the CECL process and methodologies. This auditing process has become challenging with auditors focused on loan data, expected credit loss results, and the methods used to arrive at these results. It, therefore, becomes imperative for lending institutions to monitor their loan pools regularly so that they have the relevant data ready for auditing purposes. They have to compare CECL results from one period to another to locate and rectify any issues.

Factors that can affect a loan pool are discussed below:

- When a pool involves significant product, industry, region, or borrower risk, allowance can be highly sensitive to changes in the credit environment and can result in credit losses

- Unexpected economic events such as the COVID-19 pandemic, which had a massive impact on economic activity

- Many financial institutions experienced a hike in allowance because of their exposure to the likes of dine-in restaurants, hotels, and oil exploration industries

- Credit scores are important indicators of credit risk and play a vital part in determining the interest rates for a loan

- Debt to Income (DTI) is an important indicator of risks that exist for residential loan portfolios as it has implications regarding the ability of a borrower to repay the debt based on their existing expenses versus current income

- The borrower’s payment history over a certain period of the loan can affect a loan pool and its credit risks

- Property value appreciation over life of a loan can affect the riskiness of a loan portfolio

Institutions will have to put a framework in place for the ongoing monitoring and maintenance of their loan portfolio. They can increase their profitability in the long run by pricing loans accurately at the time of origination. The risk profile of institutions will get a boost by monitoring performance over the duration of the loan. Throughout the US, loan portfolios for most credit unions and banks have evolved over decades. The collection of data for loans can be a time-consuming task for many small institutions. Conversely, institutions can become efficient at identifying risk and then save some money. Institutions need to have the ability to forensically take apart a loan portfolio and identify any relevant issues that might affect the CECL results. Lenders need to analyze a loan pool over its full cycle and leverage any information that their system might provide. Lenders can ensure the continued profitability of a loan portfolio by monitoring its performance. Financial institutions need to check current and past reports and get down to the loan level to see if anything is changing with regard to it. They need to explain to an auditor, from the bottom up, about how they have achieved their CECL results. Sometimes loans need to be individually evaluated as they no longer exhibited common risk characteristics when compared with other loans in the portfolio. CECL is an ongoing process that banks need to get right by striking the right balance between profitability and maintaining reserves for expected losses.

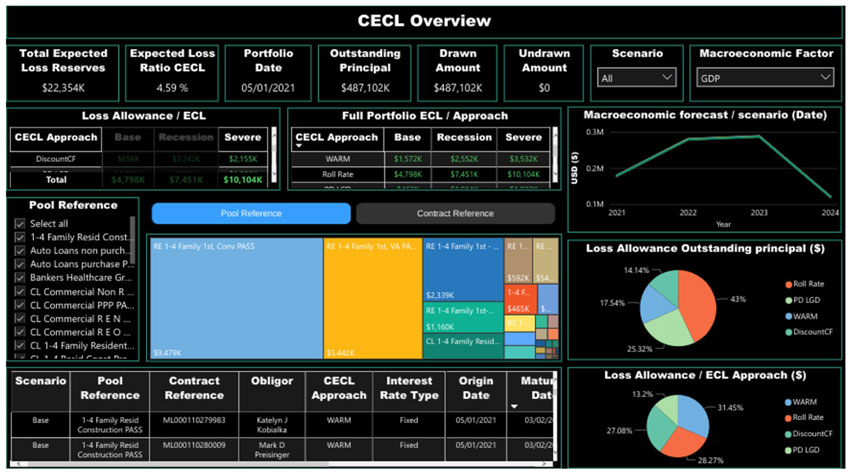

CECL Express can help…

CECL Express is a turnkey solution that fully satisfies all elements of the new CECL accounting standard. The system provides all non-loan data, including:

- Yield curves and Fed data

- Linked reports on losses from the FFIEC and NCUA

- PD and LGD curves

- Macroeconomic data

CECL Express provides more than valid ECL results. The system computes results for all methods and all loan pools, allowing the bank to optimize its CECL configuration and avoid the worst impacts of the new standard.

Banks and credit unions need to only provide the underlying loan details for the system to provide fully auditable ECL results for multiple calculation methods, including:

- Vintage

- Roll Rate

- Discounted Cashflow

- WARM

- PD/LGD

CECL Express provides more than valid ECL results. The system computes results for all methods and all loan pools, allowing the bank to optimize its CECL configuration and avoid the worst impacts of the new standard.