Q FACTORS UNDER CECL

Most financial institutions in the U.S. were left wondering about the fate of their qualitative factors, also known as Q factors, under the Current Expected Credit Losses (CECL) standard when it was issued by the Financial Accounting Standards Board (FASB) in 2016.

Bankers, faced with a 2023 CECL implementation date, wonder how best they will implement their existing Q factors to keep their allowance for credit losses figures at manageable levels. Banks and credit unions are also struggling to understand the percentage of quantitative to qualitative factors needed for their CECL calculations. The economic uncertainty caused by COVID-19 has further pushed qualitative aspects of the allowance process to the forefront of allowance estimates. A framework is now required for integrating both qualitative and quantitative dimensions into the standard Q-factors.

To meet the mandates of auditors, regulators, senior management, and investors, all qualitative allowance considerations must follow a complete, methodical, well-documented, and consistently applied approach. Most allowance models need to be supplemented with a qualitative allowance component if they are to be accurate. When compared to incurred loss models, the qualitative allowance for most institutions is likely to increase under CECL.

Qualitative allowance and its types

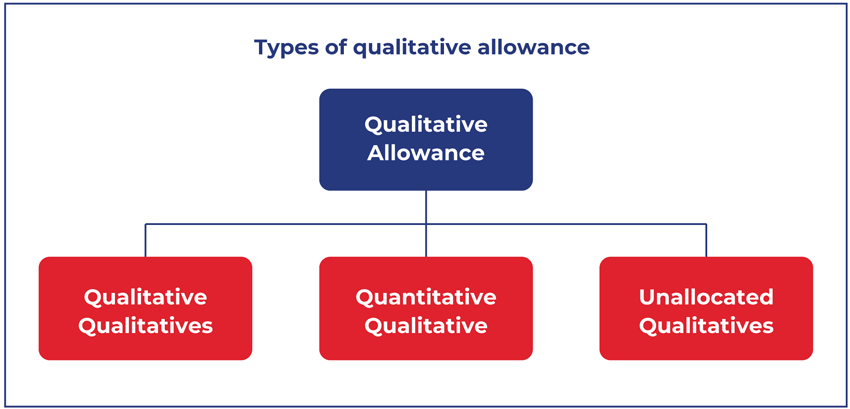

There are three types of qualitative allowances based on how the important data is compiled and consumed. They are:

- Qualitative qualitatives

- Unallocated qualitatives

- Quantitative qualitatives

- The qualitative qualitatives are that part of the qualitative allowance, which is made up of data that are subjective in nature. Given its subjective nature, auditors and regulators require a well-defined, supportable, transparent, and consistent approach.

- The quantitative qualitative allowance is that component of qualitative allowance made up of objective data pieces that can be gathered and tracked openly.

- Additional management adjustments to the allowance that are not linked to certain segments or models and do not belong withinthe framework of quantitative or qualitative qualitatives are covered by unallocated qualitatives.

Qualitative allowance application and its tiers

In some areas of the portfolio, qualitative allowance may be used more liberally than in others. We can segregate these areas into three tiers.

Tier 1:

- Off-balance sheet allowance

- New products

- Bank loans that were recently acquired,

- including purchased credit deteriorated that

- have a little history prior to acquisition

- Models that rely on data from the industry

- Portfolios that are extremely sensitive to

- model inputs

Tier 2:

- Loans that are originated and collectively

- reviewed

- Immaterial portfolios

- Portfolios that are seasoned and

- well-understood

Tier 3:

- Individually reviewed loans

Integration of qualitative factors into CECL quantitative models

Several qualitative factors will figure more prominently under CECL. These Q factors are:

- Changes in nature of the portfolio

- Changes in lending policies and procedures

- Changes in the value of underlying collateral

- for loans that are collateral-dependent

- Changes in quality of assets

- Changes in regional, international, national,

- and local economic and business conditions

Other Q factors are likely to remain unaltered from the existing incurred loss model. This is because it is difficult to incorporate them into specific quantitative model assumptions on a consistent basis. Both qualitative and quantitative criteria can be utilized to determine the appropriate degree of supplemental

qualitative allowance to be added or deducted from the allowance model output for most of the nine Q-factors.

Macroeconomic forecasts play a crucial role in CECL projection models over the expected lifetime of a portfolio. To cover management’s evaluation of each of the qualitative components, appropriate documentation is required.

Management can use qualitative allowance to supplement allowance model outputs based on their best judgment of overall economic or credit conditions throughout the forecast horizon. It is an best practice to extract the quantitative parts of any Q-factor and utilize them as a starting point in establishing any qualitative rating. To convert Q-factor ratings to genuine qualitative allowances, a rating scale is required .Documentation remains the most relevant aspect of the qualitative process for regulators ,management, and auditors.

CECL Express can help…

CECL Express is a turnkey solution that fully satisfies all elements of the new CECL accounting standard. The system provides all non-loan data, including:

- Yield curves and Fed data

- Linked reports on losses from the FFIEC

- and NCUA

- PD and LGD curves

- Macroeconomic data

Banks and credit unions need to only provide the underlying loan details for the system to provide fully auditable ECL results for multiple calculation methods, including:

- Vintage

- Roll Rate

- Discounted Cashflow

- WARM

- PD/LGD